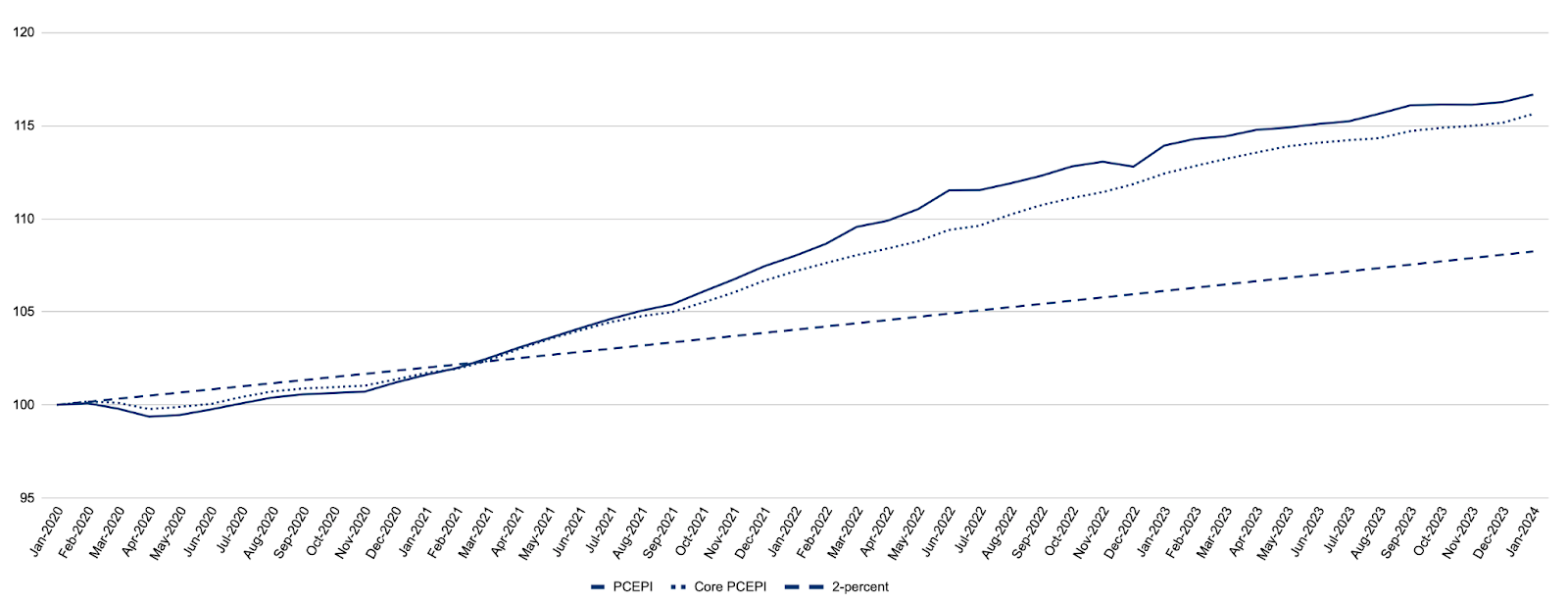

Inflation picked up in January, according to the latest data from the Bureau of Economic Analysis (BEA). The Personal Consumption Expenditures Price Index (PCEPI), which is the Federal Reserve’s preferred measure of inflation, grew at a continuously compounding annual rate of 4.1 percent in the first month of the year. The PCEPI has grown at an annualized rate of 1.8 percent over the last three months and 2.5 percent over the last six months. Prices today are 8.4 percentage points higher than they would have been had they grown at an annualized rate of 2.0 percent since January 2020.

Figure 1. Headline and Core Personal Consumption Expenditures Price Index with 2-percent Trend, January 2020 – January 2024

Core inflation, which excludes volatile food and energy prices, also increased. Core PCEPI grew at a continuously compounding annual rate of 5.0 percent in January. It has grown at an annualized rate of 2.6 percent over the last three months and 2.5 percent over the last six months.

There is no denying that measured inflation increased considerably in January. The question is whether it means inflation will likely be higher than previously expected in the months ahead. There are at least two reasons to think the January uptick is just a blip, and will be followed by much smaller price increases in the months ahead.

First, the increase in inflation was partly due to a surge in imputed prices. Imputed prices are quantified opportunity costs. What didn’t happen is not directly observed and, hence, must be estimated. Consider owner-occupied housing. Whereas the price a renter pays his landlord for housing services can be measured, the price an owner implicitly pays herself to live in her own house cannot. Economists at the BEA must estimate the price of owner-occupied housing in order to estimate the general level of prices. Similarly, some services provided by financial and nonprofit institutions serving households are not directly observable.

Although economists at the BEA surely do their best to accurately estimate imputed prices, there is no guarantee that they get it right. Correspondingly, some degree of skepticism is warranted when imputed prices diverge from market prices, as they did in January. Market-based PCE, which is a supplemental measure offered by the BEA, is based on household expenditures for which there are observable prices. It excludes most imputed transactions. The market-based PCE price index grew at a continuously compounding annual rate of 3.1 percent in January. It has grown at an annualized rate of 1.3 percent over the last three months and 2.4 percent over the last six months. Maybe imputed prices are rising more rapidly than observable prices, as estimates suggest. Or, maybe, those estimates are overstating the rise in imputed prices.

Second, the usual seasonal adjustment for January may be insufficient for January 2024. Many prices reset in January, as contracts are renewed at the start of the year. To prevent a spike in CPI inflation each January, the BEA adjusts the data to account for the typical January price increase. This procedure essentially apportions some of the increase in January prices to other months, as if the prices had grown gradually from one month to the next instead of suddenly each January.

Seasonally-adjusting price level data works pretty well in normal times. But, in unusual circumstances, the seasonal adjustment may over- or under-state actual price changes. When prices are rising faster than usual, the seasonal adjustment — which accounts for the usual increase in prices —will not apportion enough of the January price increases to other months. Consequently, the seasonally adjusted price level will tend to overstate inflation in January (and understate inflation in other months). Robin Brooks recently made this point in the context of the Consumer Price Index (CPI), but the argument applies to the PCEPI as well.

Brooks describes the January 2024 uptick in prices as “an echo of last year’s start-of-year price resets that made inflation in early 2023 look much worse than it really was.” In January 2023, the PCEPI grew at a continuously compounding annual rate of 6.7 percent. It had grown at an annualized rate of 3.5 percent over the prior three months and would grow at an annualized rate of 3.0 percent over the subsequent three months. In hindsight, January 2023 was an outlier. January 2024 looks likely to be an outlier, as well.

Following the January inflation data, most commentators fall into one of two categories: those concerned because they believe we are experiencing a resurgence of inflation, and those unconcerned because they believe the January uptick in inflation is just a blip. In contrast, I believe there is cause for concern even though the January uptick will likely turn out to be just a blip. Why? Because it will likely lead Fed officials to keep monetary policy tighter for longer.

In a recent talk, Fed Governor Christopher Waller said the January inflation data reinforced his “view that we need to verify that the progress on inflation we saw in the last half of 2023 will continue.” He said “there is no rush to begin cutting interest rates to normalize monetary policy.”

Waller rightly acknowledges that the January increase in inflation “may have been driven by some odd seasonal factors or outsized increases in housing costs.” But he errs in thinking “the strength of output and employment growth means that there is no great urgency in easing policy.” The available data is historical and monetary policy acts with a lag. To avoid overcorrecting, and pushing the economy into a recession, the Fed must ease monetary policy before the data clearly demonstrates inflation is back down to 2 percent.

The Fed failed to tighten policy swiftly as inflation picked up in the second half of 2021. Consequently, prices rose much higher than they should have. It has similarly failed to ease policy as inflation returned to its 2-percent target in 2023. The Fed should be looking ahead and adjusting monetary policy in light of its forecasts. Instead, its eyes are fixed on the rearview mirror. Let’s hope the Fed adjusts its trajectory before it is too late.

William J. Luther

William J. Luther is the Director of AIER’s Sound Money Project and an Associate Professor of Economics at Florida Atlantic University. His research focuses primarily on questions of currency acceptance. He has published articles in leading scholarly journals, including Journal of Economic Behavior & Organization, Economic Inquiry, Journal of Institutional Economics, Public Choice, and Quarterly Review of Economics and Finance. His popular writings have appeared in The Economist, Forbes, and U.S. News & World Report. His work has been featured by major media outlets, including NPR, Wall Street Journal, The Guardian, TIME Magazine, National Review, Fox Nation, and VICE News. Luther earned his M.A. and Ph.D. in Economics at George Mason University and his B.A. in Economics at Capital University. He was an AIER Summer Fellowship Program participant in 2010 and 2011.

Read “When Money Dies” by Adam Fergusson, The Nightmare of Deficit Spending, Devaluation, and Hyperinflation in Weimar Germany. From Hachette: When Money Dies is the classic history of what happens when a nation’s currency depreciates beyond recovery.In 1923, with its currency effectively worthless (the exchange rate in December of that year was one dollar to 4,200,000,000,000 marks), the German republic was all but reduced to a barter economy. Expensive cigars, artworks, and jewels were routinely exchanged for staples such as bread; a cinema ticket could be bought for a lump of coal; and a bottle of paraffin for a silk shirt. People watched helplessly as their life savings disappeared and their loved ones starved. Germany’s finances descended into chaos, with severe social unrest in its wake.Money may no longer be physically printed and distributed in the voluminous quantities of 1923. However, “quantitative easing,” that modern euphemism for surreptitious deficit financing in an electronic era, can no less become an assault on monetary discipline. Whatever the reason for a country’s deficit — necessity or profligacy, unwillingness to tax or blindness to expenditure — it is beguiling to suppose that if the day of reckoning is postponed economic recovery will come in time to prevent higher unemployment or deeper recession. What if it does not? Germany in 1923 provides a vivid, compelling, sobering moral tale.

I bet you never stopped to think what putting a 25% tariff on everything coming in from China would have on prices. Now let’s see, who did that? Oh yeah, the orange guy! Not to mention, who was it that gave out all the free money for Covid – who was the guy that wanted his name on the checks? Oh yeah, once again the orange guy! And it was the orange guy who gave tax cuts to the rich but not to the lower and middle class. Now, who was it that made things unaffordable?

For the 3rd month in a row the inflation rate has risen.

Average people tend to lose sight of how important it is to have a sound currency. It’s the difference between an easy, affordable life vs. an unaffordable and hard life with hard work and struggle.

The article exploring the potential resurgence of inflation prompts critical reflection on economic trends and their implications for consumers and businesses alike.